PM, in the NITI Aayog’s 5th Governing Council meeting held recently, called for making India a $5 trillion economy by 2024.

Here is an assessment of Foreign Direct Investment (FDI) status in India, in this regard.

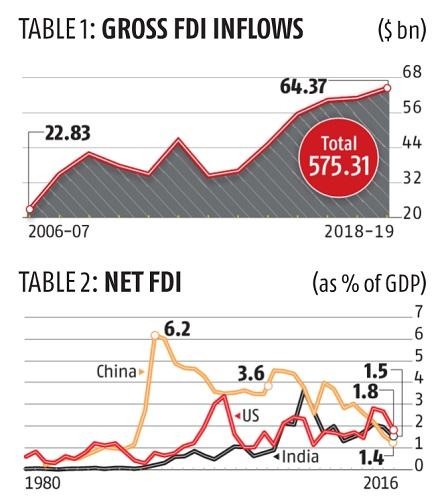

What is the current FDI scenario?

Gross inflows of foreign direct investment (FDI) rose to $64.37 billion in 2018-19.

[It was stagnated at around $60 billion for the previous two years.]

The gross FDI inflows have nearly trebled since 2006-07 when it was mere $22.8 billion.

Evidently, despite domestic economic ups and downs, foreign investors have retained faith in the Indian economy.

Net FDI inflows – It is the net FDI inflows that actually contribute towards balancing the country’s external account and boosting economic activity.

Encouragingly, net FDI inflows in 2018-19 increased to around $45 billion from around $39 billion in 2017-18.

This represents a much needed acceleration in these flows with growth rate in FY19 touching 15%.

This is in sharp contrast to the previous two years, when net FDI inflows had actually declined by (-) 6% and 6.6% respectively.

Thus, net flows in 2018-19 have staged a comeback and marginally surpassed the peak of $44.9 billion reached in 2015-16.

What do other indicators show?

Recipient of FDI flows - According to UNCTAD (World Investment Report), India is now the 10th largest recipient of FDI flows.

[The US leads the list with attracting $252 billion through FDI in 2018.]

Cross-border investment flows - India’s share in global cross-border investment flows has increased from 2% in 2010 to 3.2% in 2018.

Share in GDP - World Bank data (World Development Indicators) shows that the share of net FDI inflows in India’s GDP has less than halved over the years.

It had peaked in 1999 at 3.6% of GDP and has since then declined to stand at 1.6% in 2017.

Having staged a comeback in 2018-19, the share would be slightly higher now.

How does India compare with China?

In terms of share in GDP, India’s FDI performance looks comparable in 2017 to both China and the US.

However, now, with its GDP nearly 5 times the size of India’s economy, China managed to attract $129 billion in 2018.

Also, since its structural reforms in 1982, China has seen remarkable economic performance driven by a persistent pursuit of FDI.

Consequently, the share of net FDI inflows in Chinese GDP rose from about 0.2% in 1982 to 6.2% in 1993.

During this time, per capita incomes in China also rose from $203 to $377 and have maintained this rising trajectory.

India’s net FDI inflows as a percentage of GDP has been negligible in 1982, but increased and peaked in 2008.

But even at its peak, FDI’s share in India’s GDP was just more than half of Chinese peak levels.

Also, in 1991, per capita incomes in China and India were at somewhat similar levels (6-7%) of global average per capita incomes.

By 2018, Chinese per capita incomes were more than 85% of global averages.

On the other hand, India’s per capita incomes just reached up to 18% of the global averages over this period.

Reason - India decided to reduce the dependence on foreign investors for creating additional jobs and spurring economic growth.

It decided this at a much earlier stage compared to China.

This is one of the reasons for the low FDI levels in India.

What is to be done?

India has always had a thriving entrepreneurial community with access to domestic investible pool, generated principally by domestic household savings.

FDI finances hardly account for 5% of the country’s total investment.

Clearly, FDI inflows need to be given a special treatment over that extended to domestic investors.

India has to now discuss the relative merits and demerits of pursuing a policy that seeks to attract greenfield FDI inflows.

[Greenfield inflows - create new capacity and employment; brownfield inflows - go towards acquisition of existing assets.]

In this process, there is also the need to distinguish between “tariff jumping” versus “export oriented” FDI.

[Tariff-jumping FDI allows a foreign firm to avoid a trade barrier by locating production within the destination market.]

As widely acknowledged, the export-oriented FDI (manufacturing within) is seen to have more positive economy wide impact.

In all, a clear and consistent position has to be evolved as regards with the FDI policy, which addresses the priorities of all stakeholders.

This will ensure that there is greater predictability at all levels towards FDI.

In India’s efforts to take the economy to $5 trillion, such clarity, and a unified and predictable policy is a much needed one.