Click here for Part I and here for Part III

Why in news?

The Union Minister for Finance and Corporate Affairs, Ms. Nirmala Sitharaman tabled the Economic Su rvey 2018-19 in the Parliament.

What are the key highlights?

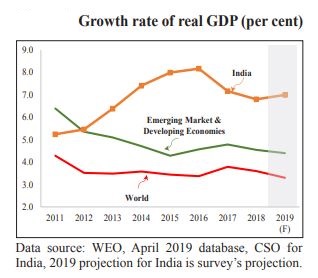

STATE OF THE ECONOMY IN 2018-19: A MACRO VIEW

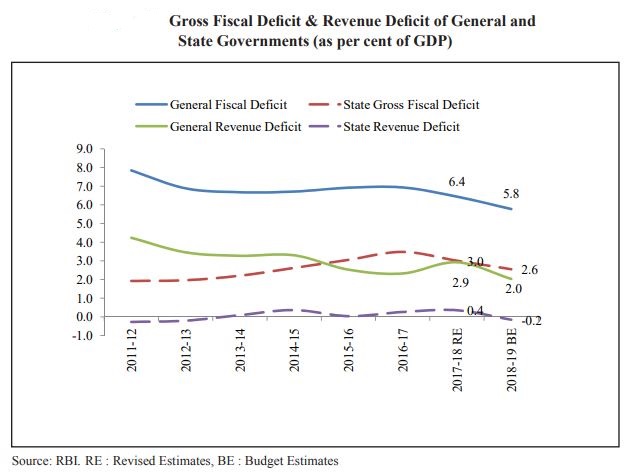

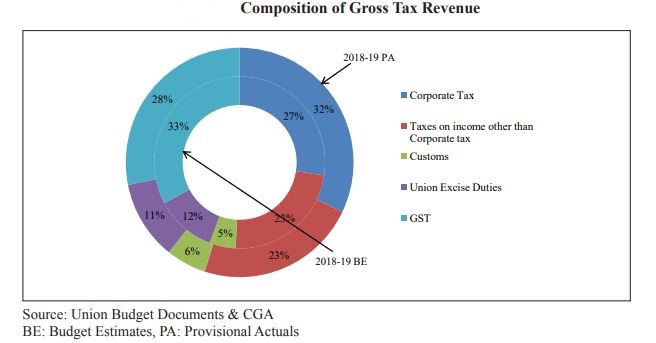

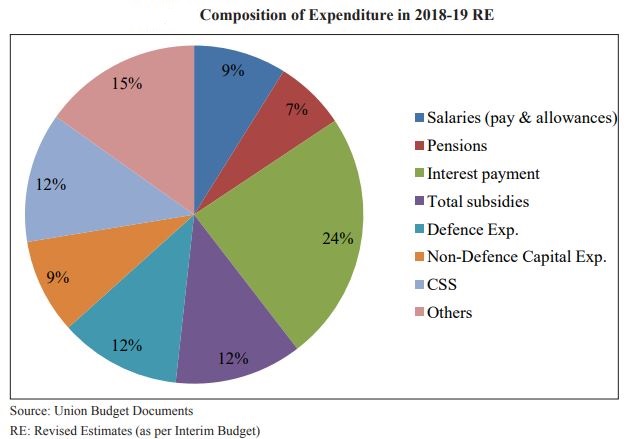

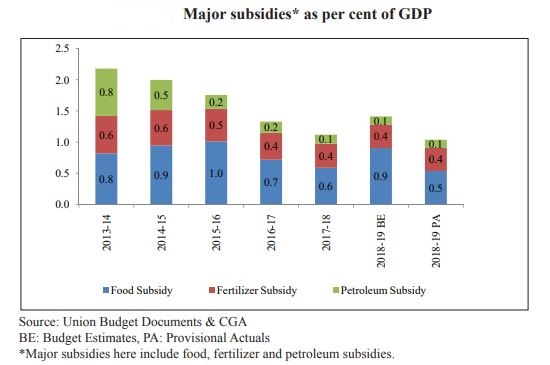

FISCAL DEVELOPMENTS

![]()

MONEY MANAGEMENT AND FINANCIAL INTERMEDIATION

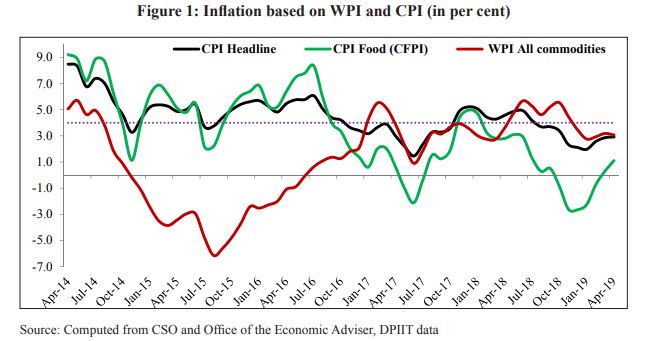

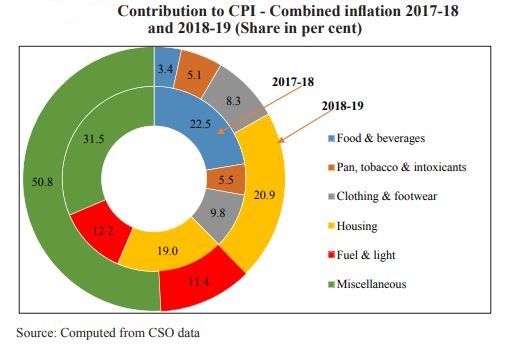

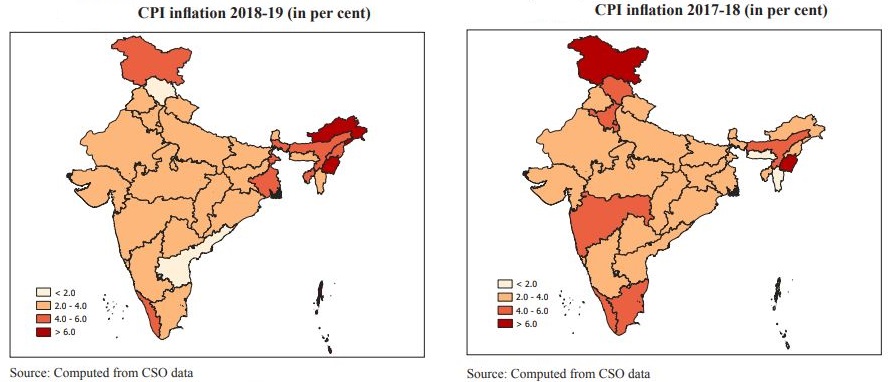

PRICES AND INFLATION

SUSTAINABLE DEVELOPMENT AND CLIMATE CHANGE

Source: Ministry of Finance website

Part III will include contents on External sector, Agriculture and Food Management, Industry and Infrastructure, Services Sector, Social Infrastructure, Employment and Human Development

Amanda Adams 5 months

Interesting summary of the Economic Survey! The GDP moderation is concerning, especially in agriculture and public administration. The investment recovery is a positive sign, but needs to be sustained. It would be helpful to see sector-specific reforms proposed. On another note, sometimes I need a break from these numbers and play Block Blast to clear my head.