The RBI’s decision to permit banks to co-lend with all registered NBFCs (including HFCs) based on a prior agreement has led to unusual tie-ups like the one between the State Bank of India (SBI) and Adani Capital.

What is theCo-Lending Model?

Co-lending or co-origination is a set-up where banks and non-banks enter into an arrangement for the joint contribution of credit for priority sector lending.

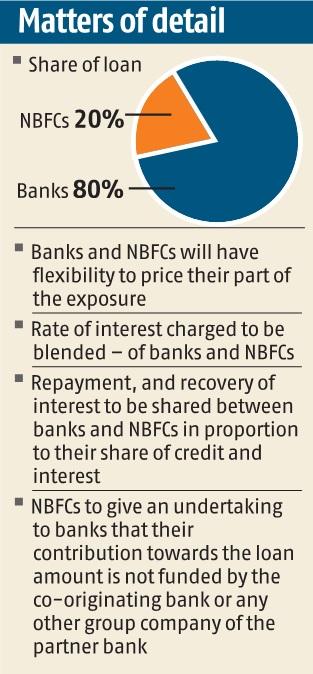

Under this arrangement, both banks and NBFCs share the risk in a ratio of 80:20 (80% of the loan with the bank and a minimum of 20% with the non-banks).

Examples- Small Business Finance (SBFC), an NBFC lending to small businesses, was one of the first NBFCs to co-originate loans with ICICI Bank in 2019.

SBI has signed a deal with Adani Capital, an NBFC of a big corporate house, for co-lending to farmers to help them buy tractors and farm implements.

IIFL Home Finance tied up with Punjab National Bank.

Gold loan NBFC Indel Money tied up with IndusInd Bank to offer gold loan in a co-lending format.

How does the co-lending model work?

The RBI had come out with the co-origination framework in 2018 allowing banks and NBFCs to co-originate loans.

These guidelines were later amended in 2020 and rechristened as co-lending models (CML) by including Housing Finance Companies and some changes in the framework.

Aim of CLM- To improve the flow of credit to the unserved and underserved segment of the economy at an affordable cost.

As per RBI norms, a minimum 20% of the credit risk by way of direct exposure shall be on NBFC’s books till maturity and the balance will be on the bank’s books.

Upon maturity, the repayment or recovery of interest is shared by the bank and NBFC in proportion to their share of credit and interest.

NBFCs act as the single point of interface for the customers and a tripartite agreement is done between the customers, banks and NBFCs.

What are the opportunities?

Ensures delivery of credit to the unserved and underserved

Help digital lending start-ups and mid-size NBFCs to join their strength of distribution with bank’s funds

Aid banks in expanding the customer base as NBFCs have reach in tier-3 and tier-4 cities

What are the hurdles in co-lending?

IT integration of systems is a major problem as both banks and NBFCs would operate on different systems, different underwriting processes and parameters.

There are concerns about the longevity of the relationship between the banks and NBFCs as the co-lending model is still in the nascent stages.

Most of the mid-sized well-rated NBFCs still opt for term loans over entering into co-lending models, given the complexities around integration and processes.

Since 80% of the risk will be with the banks, they will take the big hit in case of a default.

While the RBI hasn’t officially allowed the entry of big corporate houses into the banking space, NBFCs floated by corporate houses now have more opportunities on the lending side through direct co-lending arrangements.

What is the way forward?

To address the huge credit gap the co-lending model is one of the right ways to go forward, but challenges around tech integrations and ground-level executions should be addressed.

As the economy recovers coupled with pent-up demand, these kinds of models will evolve and grow to fulfill the credit requirements of the priority sector segments.