Recently, Gross Non-Performing Assets(NPAs) have fallen, but emergence of fresh NPAs and unsatisfactory recoveries needs banks intervention.

What are NPAs?

NPA - An asset becomes non-performing when it ceases to generate income for the bank.

It is a loan or advance for which the principal or interest payment remained overdue for a period of 90 days.

Types - Banks are required to classify NPAs into Substandard, Doubtful and Loss assets.

Substandard assets - Assets which has remained NPA for a period less than or equal to 12 months.

Doubtful assets - An asset would be classified as doubtful if it has remained in the substandard category for a period of 12 months.

Loss assets - Loss asset is considered uncollectible and of such little value that its continuance as a bankable asset is not warranted, although there may be some salvage or recovery value.

What is the trend in NPAs?

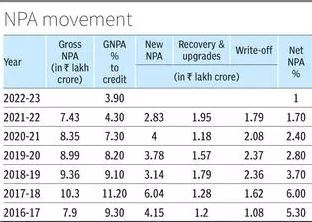

There is a decline in gross non-performing assets (GNPA) ratio of Indian banks.

In 2017-18, this ratio was as high as 11.2 % raising concerns on the stability of the banking system.

In 2022-23 GNPA ratio declined to 3.9%, there has been significant write-offs since 2016-17 amounting to ₹10 lakh crore.

During last three years (2019-22) alone fresh NPAs add up to ₹10.61 lakh crore

What is loan write-off?

A loan write-off is a tool used by banks to clean up their balance-sheets. It is applied in the cases of bad loans or non-performing assets (NPA).

If a loan turns bad on the account of the repayment defaults for at least three consecutive quarters, the loan can be written off.

By writing-off a loan, the banks set free the money parked for the provisioning and utilise the amount for business (it will no longer be counted as an asset).

Lost inventory, unpaid debt obligation, bad debts, and unpaid receivables are also written off.

In the cases of NPA, 100 % provisioning is required in accordance with the Basel-III norms.

Some recent data show that private banks have been more active in writing off NPAs than public sector banks (PSBs).

Tax benefits- Lenders become eligible for a tax rebate on the total loan value by writing them off.

Loan provisioning- By writing-off loans, lenders don’t need to release the remaining limit to defaulting borrowers.

Doing this helps them release funds previously blocked for a borrower.

They can use these to provide loans to others in need or for their business.

Right to recover- Lenders don’t lose the right to recover outstanding loans even after writing them off.

They can use the means necessary to recover the full or partial loan amount.

Governance-Writing-off loans help lenders maintain a clean and updated balance sheet, it results in significant decline in NPAs.

How to prevent NPA accumulation?

Revisit business models- Banks needs to revisit business models as fault-lines would lead to higher NPAs and credit losses.

Ideally, from lending perspective, banks need as many business models as credit segments and customer segments.

Governance - The layers of governance such as business, risk and operational governance must be regulated along with corporate governance.

Fine tune risk appetite- It is the amount of risk the lender is willing to undertake.

It needs to be aligned with risk culture, underwriting skills in a particular domain and risk tolerance.

Check fund diversion- The diversion of funds in corporate lending is more widespread and intense.

Bank collaboration is needed to detect the practice and find a remedial solution for the same.

Increase NPA recoveries- NPA recoveries is low around 25 % of the claim amount.

Even under the Insolvency Bankruptcy Code 2016, regime the recovery rate has fallen from 45 % to 23.8 %.

The government, regulators and lenders need to rework these recovery/resolution frameworks.

Need of skilled expertise- Underwriting skills and turnaround skills require high expertise because the changes in industry and real economy are quite fast and global.