Recently Reserve Bank of India has ordered Paytm Payment Bank to halt most of its business.

Payment Bank

A payments bank is a new category of banks conceptualized by the Reserve Bank of India, which operates at a smaller scale than an actual bank and doesn’t involve any credit risk.

Aim- To provide saving accounts to those who are not able to create a savings account as they are afraid to pay heavy maintenance.

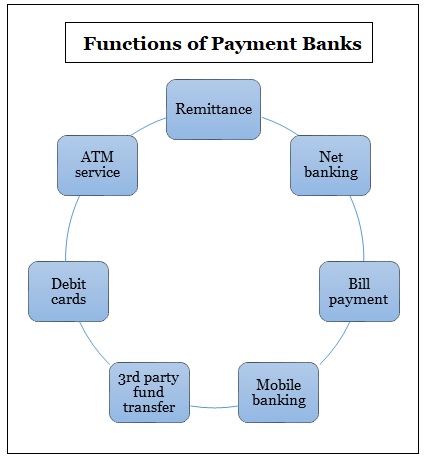

Operation- The bank operate digitally (on mobile phones and other devices using the internet) rather than through physical branches.

Provision of credit- It provides credit to smaller units such as low-income household, migrant labour workforce, small business units and unorganized sectors.

Limited services- These banks cannot carry out lending activities like

Advancing loans

Issuance of credit cards etc.,

What is the issue?

Paytm Payments Bank (PPB) has been facing scrutiny from RBI since 2018, due to concerns on Know Your Customer compliance and Information Technology related issues.

Need of regulation- RBI has found PPB to be in violation of its rules and regulations such as the ceiling on customer deposits, the reporting of suspicious transactions, and the compliance with the Foreign Exchange Management Act.

RBI has reportedly accused Paytm of financial crimes, including falsifying customer information and money laundering.

New guidelines-RBI has asked Paytm to stop all services offered by its banking division, also known as the wallet service, due to "persistent non-compliance" of its rules.

It has asked the company to stop accepting deposits into people's Paytm bank accounts, or wallets, from March 1, 2024 although customers would be allowed to continue making payments until the balance in their accounts is exhausted.

The app can continue to facilitate quick payments between non-Paytm bank accounts as an intermediary but it can’t accept direct deposits.

This would seriously impact the company’s wallet business as its wallet offers various services like deposits, make deposits and keep money.

It affects the customers of Paytm Wallet, Paytm FASTag, and other services offered by Paytm Payments Bank.

Customers can use their existing balance till it is exhausted, but cannot add any money or conduct credit transactions after February 29, 2024.

Alternative- There are over 20 banks and non-banking entities that offer wallet service. The leading one after PPBL wallet includes Mobikwik, PhonePe, SBI, ICICI Bank, HDFC, Amazon Pay etc.,

There are 37 banks comprising all the known public and private sector banks like SBI, HDFC etc., which are authorised to provide FASTag.

How payment banks are regulated by RBI?

Scheduled banks- The payments banks are given the status of scheduled banks under Reserve Bank of India Act, 1934.

However, the words “Payments Bank” have to be used by the companies in their name in order to differentiate it from other banks.

Registration- They will be registered as a public limited company under the Companies Act, 2013.

License provision- They are licensed under Banking Regulation Act, 1949.

Regulation- It will be governed by the provisions of the Banking Regulation Act, 1949, Reserve Bank of India Act, 1934, Foreign Exchange Management Act, 1999, Payment and Settlement Systems Act, 2007, Deposit Insurance and Credit Guarantee Corporation Act, 1961 and other relevant Statutes and Directives.

Guidelines- RBI issues specific guidelines that outline the eligibility criteria, permissible activities, capital requirements, and other operational aspects for entities seeking to operate as payment banks.

Ownership and capital requirements- The entities intending to establish payment bank must adhere to these regulations to ensure financial stability and the ability to carry out banking operations effectively.

Customer protection- Payment banks are required to implement robust KYC procedures to verify the identity of their customers and prevent money laundering and fraudulent activities.

Security standards- Payment banks are expected to adhere to high technology and security standards to ensure the safety and integrity of financial transactions.

Reporting- Payment banks are required to submit periodic reports to the RBI, providing details about their financial health, operations, and compliance with regulatory norms.

Review- RBI involves in regular inspections, audits, and assessments to ensure that these entities comply with regulatory guidelines and maintain financial stability.