Since most of the co-operative credit societies avoid regulatory oversight and indulge in risky lending, their supervision needs to be tightened.

What are co-operative credit societies?

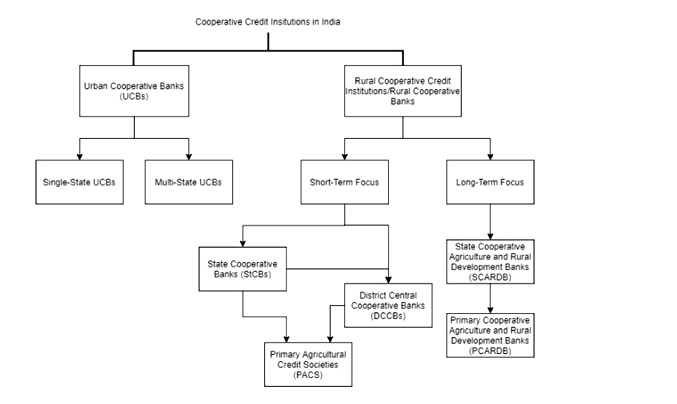

Co-operative credit societies are formed to provide financial support to the members.

The society accepts deposits from members and grants them loans at reasonable rates of interest in times of need.

They are registered and regulated by the Registrar of Co-operative Societies of the respective State governments and by the Central Registrar of Co-operative Societies if these entities function in more than one State.

Village Service Co-operative Society and Urban Cooperative Banks are examples of co-operative credit society.

What was the RBI’s advisory on co-operative credit societies?

The RBI cautioned the public against some co-operative credit societies using the word “bank” in their names.

It has been clarified that these entities aren’t allowed to perform banking activities, as per the Banking Regulation Act, 1949, through acceptance of deposits from non-members, and nominal or associate members.

Their deposits are not protected under the deposit insurance cover of DICGC.

The RBI mentioned the violation of Section 7 of the Banking Regulation Act while bringing in the amendments introduced by the Banking Regulation (Amendment) Act, 2020.

A similar press release was issued on November 29, 2017 in reference to Section 7 of the Banking Regulation Act (As Applicable to Co-operative Societies) only.

The RBI has over the years been tightening regulations governing cooperative banks, having cancelled the licences of at least 6 of them and issuing over 200 directives.

What are the problems plaguing the co-operative credit societies?

Accepting deposits from non-members -Some cooperative societies are accepting deposits from non-members/ nominal members/ associate members is in violation of the provisions of the Banking Regulation Act.

Regulation - These societies do not come under the RBI scanner despite accepting deposits from and disbursing loans to their members.

While those co-operative credit societies with reserves and paid-up capital of over Rs 1 lakh have to seek a licence from the RBI, most of them operate with a lower capital to avoid regulatory oversight.

State governments continue to control the smaller cooperative banks while the RBI too oversees the operations of such institutions and this dual regulation causes confusion.

Opaque laws – Co-operative credit societies are governed by opaque and anachronistic laws and their customers stand to lose if these societies go bust.

Some of the societies registered under the Multi-State Co-operative Societies Act, 2002 have reportedly garnered public deposits running into thousands of crores during the last 10 years.

Advertisements of high interest rates – If co-operative credit societies offer exorbitantly high interest rates on the deposits compared to banks, the interest rate of lending would be higher and raises questions on who would be the borrowers.

This requires the societies to lend to risky borrowers which will totally affect the health of the financial sector.

Domino effect - Since these societies have very thin base of capital and reserves, any failure could prompt domino effect.

Depositors - Since these societies are not subject to Know Your Customer rules and anti-money laundering laws, money launderers could be the potential depositors.

Undue advantage - There is also another warning that some societies are taking undue advantage of the poor in financially excluded areas and exploiting them leading to financial exclusion.

Others- Poor governance, light-touch regulation, local political intervention and a change in the composition of the banking industry leading to tight competition are all factors impacting the cooperative banking industry.

How can theco-operative credit societies be improved?

Ill-functioning societies need to be isolated and special precautionary investigations must be held by the controllers and supervisors.

If the RBI has definite information on societies circumventing the provisions of Section 7 of the Banking Regulation Act, appropriate legal action must be initiated against the wrongdoers to protect the interests of depositors.

Member-depositors should be first concerned about the safety of their principal and then the return thereon.

Internal surveillance mechanism has to improve substantially and the State governments along with RBI can regulate and supervise these societies.