As per the government, during the last five years (2017-18 to 2021-22), scheduled commercial banks wrote off non-performing assets (NPAs) worth Rs 9,91,640 lakh crore.

What is the RBI data on loan write-offs?

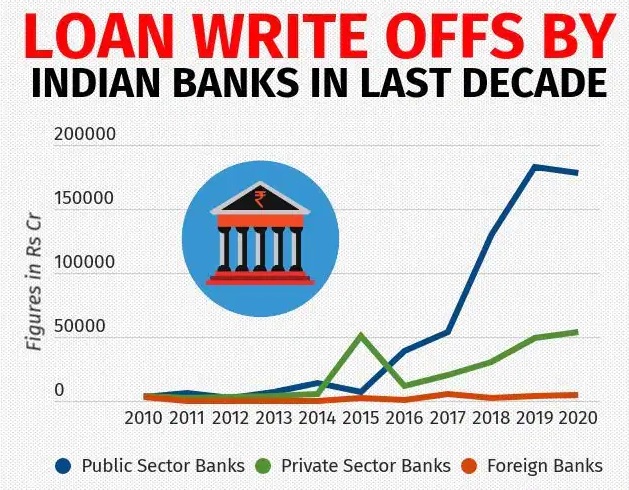

According to RBI data, banks have written off Rs 10,09,510 crore over the last five years.

Public Sector Banks (PSBs) accounted for most of these write-offs.

Banks were able to recover only 13 % of this amount subsequently despite lending funds against assets or collaterals.

What are the causes for losses in banking / financial sector (BFSI)?

Major causes for losses in banking / financial sector (BFSI) include

Economic downturn

Technological disruption

Change in government policies

Regulatory hurdles

Increased competition

Fraud or malfeasance

Banker’s error of judgement in advancing funds

What does loan write-offs mean?

Loan write-offs - Writing off a loan essentially means it will no longer be counted as an asset.

Significance - By writing off loans, a bank can reduce the level of non-performing assets (NPAs) on its books.

The amount so written off reduces the bank’s tax liability.

Reason - The bank writes off a loan after the borrower has defaulted on the loan repayment and there is a very low chance of recovery.

It may be important to realise that all loan write-offs are not lost money.

Many write-off cases continue to be on birth register of banks/financial institutions.

Write-off is resorted to even in cases where the bank has not exhausted all avenues for recovery of dues.

Such write-offs do not affect the right of the bank to proceed against the borrowers to collect the dues.

Any recovery made against the borrower is considered as a profit for the bank in that financial year.

Why loan classification is so significant?

Loan classification reflects what the true value of the loan might be.

It is accompanied by provisioning, which ensures the bank sets aside a buffer to absorb likely losses.

If the losses do not materialize, the bank can write back provisioning to profits.

If the losses do materialize, the bank does not have to suddenly declare a big loss, it can set the losses against the prudential provisions it has made.

The bank balance sheet then represents a true and fair picture of the bank’s health.

Quick Facts

Non-performing assets (NPAs)

NPA is a loan or advance for which the principal or interest payment remained overdue for a period of 90 days.

Banks are required to classify NPAs further into Substandard, Doubtful and Loss assets.

Substandard assets - Assets which has remained NPA for a period less than or equal to 12 months.

Doubtful assets - An asset would be classified as doubtful if it has remained in the substandard category for a period of 12 months.

Loss assets - Loss asset is considered uncollectible and of such little value that its continuance as a bankable asset is not warranted, although there may be some salvage or recovery value.