The RBI has issued a fresh set of rules for non-banking finance companies (NBFCs) which limits lending to IPO investors to Rs 1 crore per borrower from April 1, 2022.

What is an Initial Public Offering (IPO)?

An initial public offering (IPO) refers to the process of offering shares of a private corporation to the public in a new stock issuance.

Companies must meet requirements by exchanges and the Securities and Exchange Commission (SEC) to hold an IPO.

IPOs provide companies with an opportunity to obtain capital by offering shares through the primary market.

How does IPO funding work?

IPO Funding is a loan offered for applying in primary stock market by NBFC's to high net worth individuals (HNI).

The investor pays only small margin for applying in IPO and rest amount is funded by the lender.

Interest is charged between 8 to 12% and it varies by the lender.

Through IPO Funding, an investor can leverage its own funds in primary market and thereby maximize the profits in a very short span of time.

IPO Funding loans are short term loans, where in most cases they are for 7 days, from the IPO closing day to date of listing of IPO shares.

Repayment of these short term loans is up to 3 months.

What are the advantages of IPO funding?

Investor can apply for more shares, thus increasing the chances of a large allotment.

Offers good opportunity to make huge profits in a short span.

Only small amount of margin is needed which increases the profits multifold.

Funding cost came down significantly in recent time because of quick IPO listings and reduced interest rates.

Simple Documentation and streamlined speedy processing of loans.

What are the concerns of IPO funding?

It is a high risk high reward investment that could result in to massive losses.

Since investor pays only small amount of margin money, the losses could be multi fold.

It is not for investors applying in retail category.

Borrowing limit varies as per the scheme launched for the IPO, and on the level of subscription under the HNI category.

Interest rate varies as per the scheme launched for the IPO, and is charged upfront.

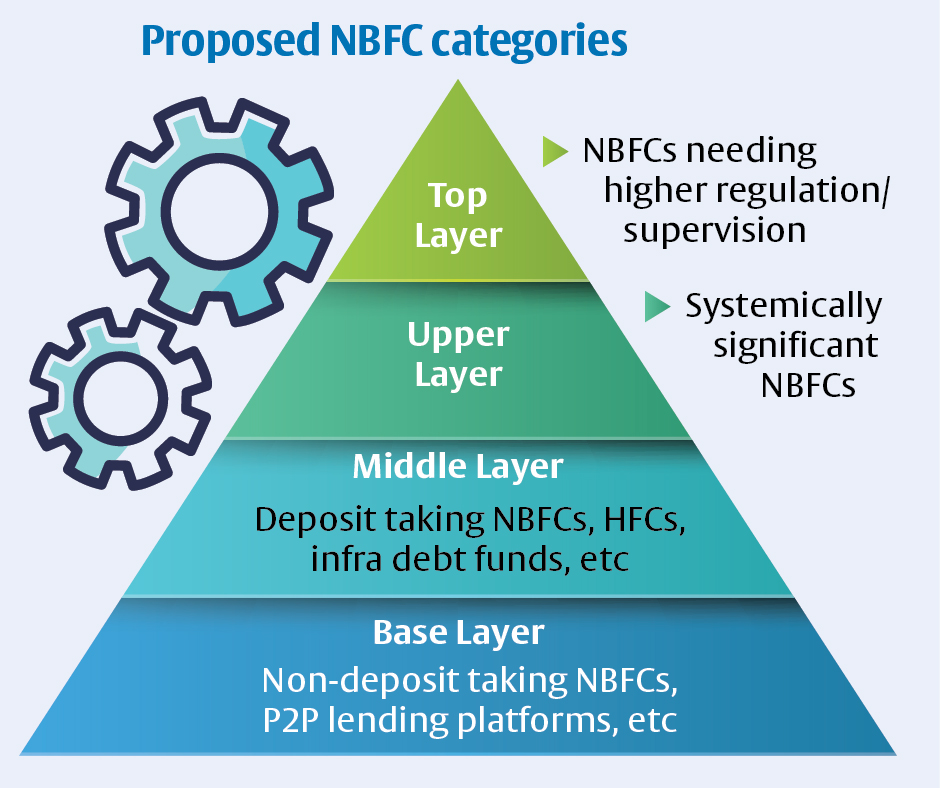

What is the new RBI framework?

Layer-based structure - Under the new framework, the regulatory structure for NBFCs shall comprise four layers — base, middle, upper and top layer.

The first category primarily entails non-deposit taking NBFCs with less than Rs 1,000 crore in assets.

The second category includeall deposit taking NBFCs irrespective of asset size.

The Upper Layer will comprise the top ten eligible NBFCs in terms of their asset sizes.

Depending on sudden risk factors, the RBI can move Upper Layer companies to the Top or fourth category, citing systemic risks.

Sensitive exposure – Exposure to the capital market and commercial real estate shall be the sensitive exposure for NBFCs.

The RBI has proposed sensitive sector exposure norms for NBFCs in the middle and upper layers.

Minimum net owned fund - The regulatory minimum net owned fund for NBFC-Investment and Credit Companies, NBFC-MFI and NBFC-Factors shall be increased to Rs 10 crore by March 2027.

Management of NBFC affairs - At least one of the directors should have relevant experience of having worked in a bank or an NBFC.

Why has the RBI come out with this rule?

Non-banks are able to borrow funds at 4-5 % and interest rates on such loans have dropped to 7-8 %.

Leveraged IPO bids unfairly tilt the allotment process in favour of short-term bettors removing the genuine long-term investors and distorting price discovery.

The new rule aims to moderate the over-subscription numbers and listing gains.

The RBI aims to put the NBFCs on line with banks that already has Rs.10 lakh limit.

What implication will the RBI rule have for upcoming IPOs?

The new rules might reduce the quantum of funds available with high networth investors (HNI) for bidding in IPOs.

The number of oversubscriptions in the HNI category will come down which will benefit the price discovery process.

The NBFC sector has undergone considerable evolution in terms of size, complexity, and inter-connectedness and hence there is a need to align the regulatory framework for NBFCs.