The monetary policy committee of Reserve Bank of India has unanimously decided to cut lending rate by 35 bps.

The central bank also lowered its GDP growth projection from 7% in June policy to 6.9% now.

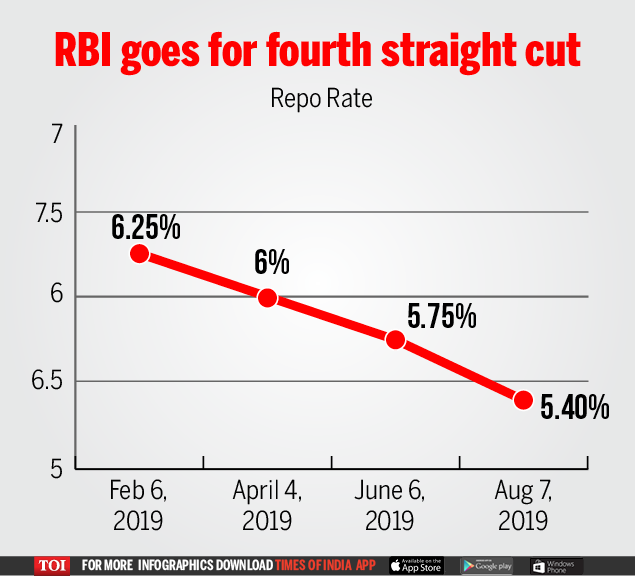

What is the repo rate?

Repo rate is the rate at which RBI lends to commercial banks.

With a 35 basis point cut (highest this year), the repo rate stands at a 9-year low of 5.4% since July 2010 when it was 5.25%.

The current rate cut is the fourth this year. The previous three cuts this year were 25 basis points each.

What is the rationale?

The rate cut comes as a move to boost economic activity amidst slowing consumption demand.

Inflation is a key consideration for a rate cut and it was a key factor for the RBI to go for a rate cut now.

The monetary policy statement mentioned that inflation was currently projected to remain within the target over a 12-month ahead horizon.

But besides this, the decision was also taken to boost aggregate demand especially private investment.

What were the RBI’s observations?

The RBI statement further said that domestic economic activity continues to be weak.

This is because of the global slowdown and escalating trade tensions posing downside risks.

It noted that private consumption, the mainstay of aggregate demand, and investment activity remain sluggish.

However, the favourable inflation outlook provides enough space for policy action to close the negative output gap.

Addressing growth concerns by boosting aggregate demand, especially private investment, assumes the highest priority at this juncture.

Why is the GDP growth revision now?

This is the second consecutive policy statement where the RBI has lowered its GDP growth projection for 2019-20.

In June 2019 statement, it revised it projection downward from 7.2% (stated in April 2019) to 7%.

This time it further revised the growth projection further down to 6.9%.

The downward revision is primarily because various high frequency indicators suggest weakening of both domestic and external demand conditions.

Business expectations Index of the Reserve Bank’s industrial outlook survey shows muted expansion in demand conditions in Q2.

Nevertheless, a decline in input costs augurs well for growth.

The RBI said that the monetary policy easing since February 2019 is expected to support economic activity, going forward.

How does the future look?

Despite three consecutive rate cuts aggregating to a total of 110 basis points, the transmission by banks to lenders has not been even a third of this.

The central bank says that banks have passed on just 29 basis points which is poor indeed.

One factor inhibiting transmission was the tight liquidity conditions until June 2019.

Since June, the RBI has eased the liquidity norms; the last two months the central bank has in fact had to absorb excess liquidity floating around.

There is, therefore, reason to hope that transmission from hereon would be quicker.

What is the way forward?

A rate cut alone will not suffice as the cost of capital is just one aspect that determines investment.

The government has to play its part too in boosting growth and roll out measures at this front.

Arguably, the space for fiscal concessions is limited given the overall revenue scenario.

The slowdown now is part cyclical which can be addressed by a rate cut and part structural, for which reforms are an absolute necessity.

The government can certainly push for further reforms to incentivise investment without affecting its fiscal arithmetic.