Sri Lanka has reached a staff-level agreement (formal arrangement) with the IMF that promises access to 29 billion dollar over a 4-year period.

What is the case with Sri Lanka?

Sri Lanka’s economic crisis- Sri Lanka’s economic situation has worsened with 51 billion dollars of external debt.

So, the country has reached an agreement with IMF to access credit under IMF’s Extended Finance Facility.

Conditions- It comes with a host of conditions varying from

Raising fiscal revenue

Reducing corruption vulnerabilities

Safeguarding financial stability

Persuading the country’s multiple creditors to restructure and reschedule past debt

Significance- The agreement is a step towards convincing foreign creditors and investors to return to the country.

Steps taken- The Central Bank has

Floated the rupee

Raised interest rates sharply

Increased electricity tariffs and fuel prices

Restored tax cuts

What are the challenges?

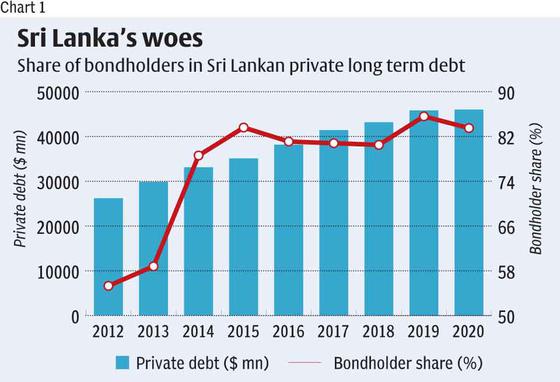

The outstanding long-term debt had risen from 26.2 billion dollar from 2012 to 46 billion dollar in 2022.

The share of private creditors had risen to 37%.

The bondholders in private credit had risen to 84%.

Private bondholders would be less willing to accept any deal that requires them to take some losses.

Talks with International Sovereign Bond (ISB) holders is a more complex exercise, with geopolitical dimensions.

How can Sri Lanka’s crisis be compared with other countries?

Similiarities- Private long-term external debt outstanding of countries identified by the World Bank belonging to the low and middle income category more than doubled from 2012 to 2020.

The share of bondholders in that debt rose from 63% in 2013 to 80% in 2020.

Differences- The variation is based on bond-based borrowing by government in the different regions.

Overall, the share of governments in foreign currency bond issues across emerging market and developing economies (EMDEs) has fallen between 2002 and 2021.

The fall has been largely driven by declines in developing Europe and Latin America and the Caribbean.

The share of government issuance has risen in Africa and the Middle East and in developing Asian and the Pacific.

But foreign currency bonds may not be the best channel to mobilise resources as foreign borrowing requires debt service commitments to be covered in foreign currency.

Increased dependence of less developed nations on sovereign bondholders has not only contributed to a debt crisis but made resolution near impossible.