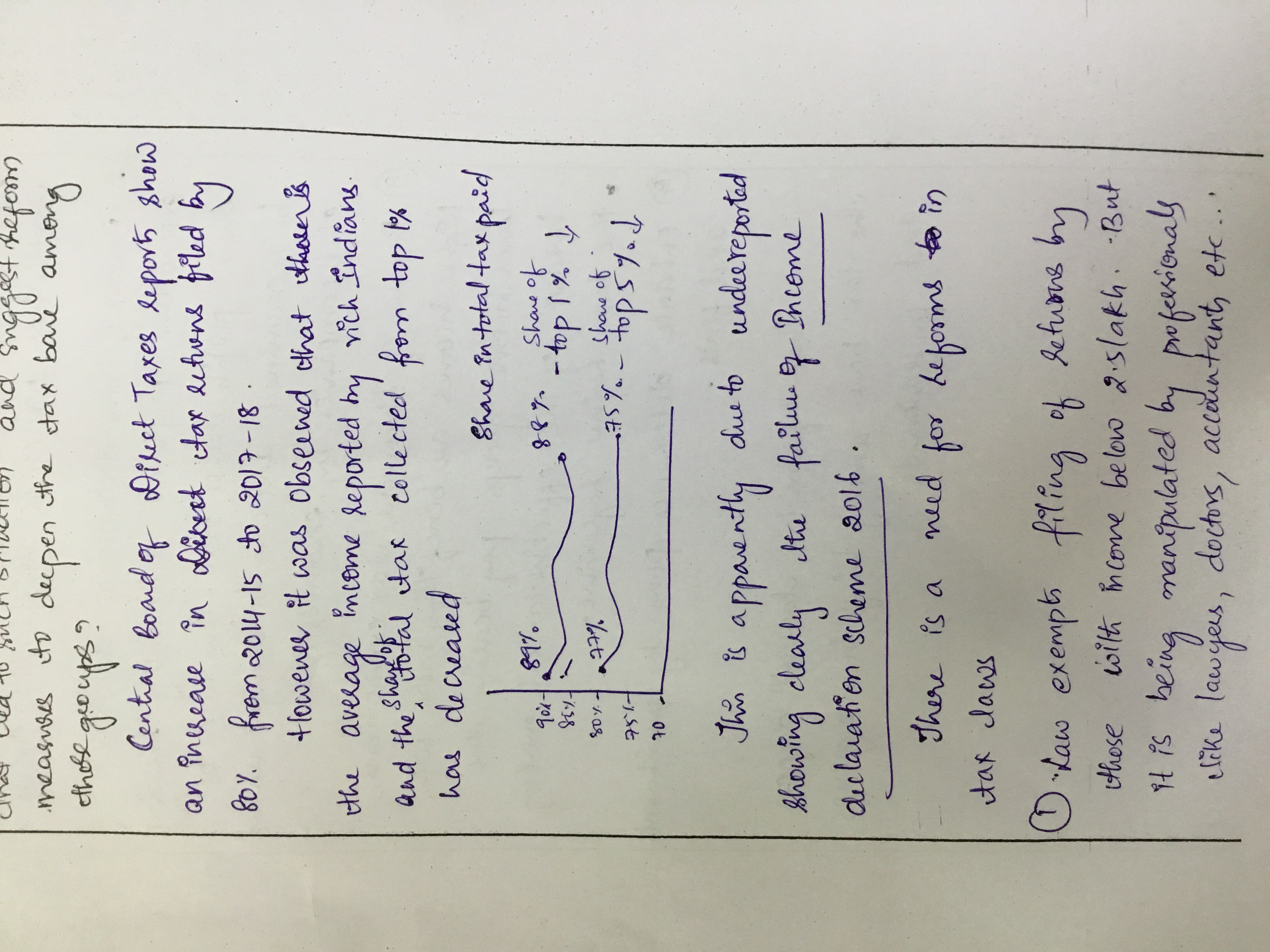

Tax evasion and avoidance is widespread among the high-income groups and big corporates in India. Examine the loopholes in Indian tax laws that led to such situation and suggest reform measures to deepen the tax base among those groups. (200 words)

Refer – The Hindu

Enrich the answer from other sources, if the question demands.

IAS Parliament 6 years

KEY POINTS

Loopholes & Reform measures

· Individuals – The present tax law does not require filing of returns if the income is below the taxable threshold (Rs. 2.5 lakh).

· This means that many professionals who can easily manipulate their accounts never appear on the radar of the taxman.

· The law should mandate filing of returns by all professionals and proprietorship businesses regardless of their profit.

· This will increase compliance by enabling the taxman to scrutinise suspicious cases.

· There is also a re-introduction of the wealth tax since the wealth level is harder to manipulate and the tax is harder to evade compared to income.

· Companies – The tax law allows offsetting of past losses against future profits for companies and the definition of admissible expenditures in the law are susceptible to easy manipulation.

· These provisions are widely misused by corporates by claiming bogus expenses, to artificially reduce their profit and hence their tax liability.

· A large number of companies showing negligible or no profit points to a continued prevalence of shell companies and other dubious structures which require systematic investigation.

· Moreover, the numerous tax exemptions also come in handy for tax avoidance and big corporates benefit more from these exemptions.

· Consequently, smaller companies face a higher effective tax rate compared to larger corporates which makes the tax regime regressive.

· Administration – There is also a need to enhance the deterrence power of the law, which depends on the likelihood of punishing tax evaders along with imposing a fine.

· At present, the Income Tax Department has a very poor win rate before the appellate tribunal and the higher judiciary and the law does not bite enough to hurt the tax offender.

· The odds of punishing the offenders can be increased by integrating the GST, the income tax and the Ministry of Corporate Affairs’ databases.

· These measures will go a long way in deepening the tax base among high-income groups and professionals.

Nandadeep 6 years

Please review.Thanks

IAS Parliament 6 years

Sahitya 6 years

Please review

IAS Parliament 6 years